I. Conceptual Framework

The Mineral Accounts of the Philippines is a publication that presents the physical asset accounts for nickel, chromite, copper, and gold. This is an update of the pilot compilation under the Philippine Wealth Accounting and the Valuation of Ecosystem Services (Phil-WAVES)1 project.

The System of Environmental-Economic Accounting (SEEA) 2012 – Central Framework2, a multi-purpose framework for measuring the environment and its interaction with the economy, serves as the framework for this study. It is also a statistical framework that consists of a comprehensive set of tables and accounts which guides the compilation of consistent and comparable statistics and indicators for policymaking, analysis, and research.

The SEEA Central Framework covers measurement in three main areas: (1) the flows of resources within the economy and between the economy and the environment; (2) the economic activity and transactions related to the environment; and (3) the stocks and the changes in stocks of environmental assets, such as mineral resources, which is the main focus of this study.

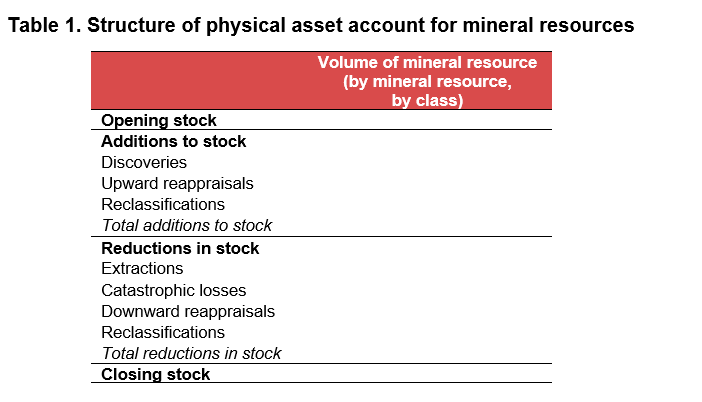

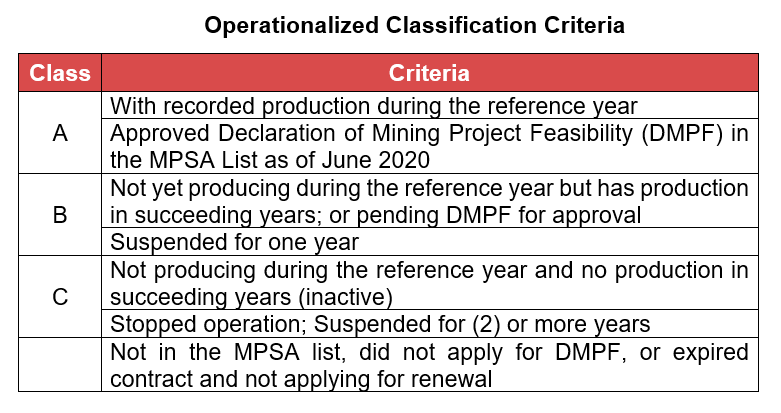

The accounts provide information on the available stocks of these metallic minerals at the start and end of each year, as well as the changes that occurred during the period. These mineral resources were also classified following the United Nations Framework Classification for Fossil Energy and Mineral Resources (UNFC-2009) as follows: Class A, commercially recoverable resources; Class B, potentially commercially recoverable resources; and Class C, non-commercial and other known deposits.

A basic physical asset account for mineral resources is compiled by type of resources, each with the same unit of measurement, and by class of resources.

II. Data Sources

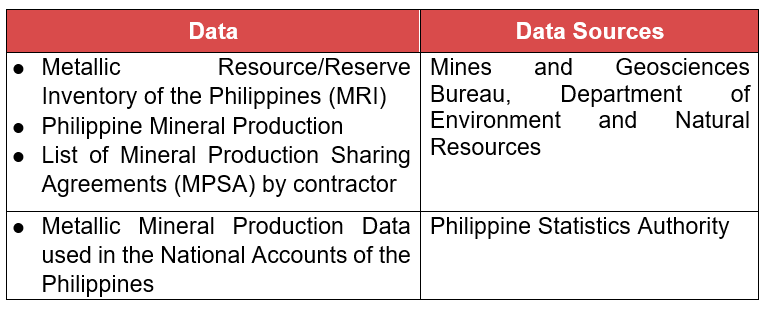

The data for estimating the physical asset accounts were gathered from the following:

III. Estimation Methodology

1. Consolidated data from the MRI from Mines and Geoscience Bureau.

2. Performed data cleaning and combined lines referring to the same year, and same contractor.

3. Encoded production data, and set up physical accounts by contractor.

4. Determined the year of discovery using the list of Mineral Production Sharing Agreement, the first record in the MRI or one year before the first production, whichever is applicable.

5. Estimated the opening stocks, closing stocks and reappraisals (balancing item using residual method) based on the available data, and determined the appropriate class using the criteria discussed below.

6. Determined the timepoints when reclassifications occurred, and the corresponding stocks for each contractor.

7. Consolidated the results by class.

IV. Definition of Terms

a. Asset is a store of value representing a benefit or series of benefits accruing to an economic owner by holding or using the entity over a period of time. It is a means of carrying forward value from one accounting period to another.

b. Environmental assets are the naturally occurring living and non-living components of the Earth, together constituting the biophysical environment, which may provide benefits to humanity.

c. Individual environmental assets are those assets that may provide resources for use in economic activity. They comprise mineral and energy resources, land, soil resources, timber resources, aquatic resources, other biological resources, and water resources.

d. Catastrophic losses rarely occur with mineral resources. Catastrophes such as collapsing of mines may occur but this does not reduce the stocks of the resources.

e. Depletion, in physical terms, is the decrease in the quantity of the stock of a natural resource over an accounting period that is due to the extraction of the natural resource by economic units occurring at a level greater than that of regeneration.

f. Discoveries are additions representing the arrival of new resources to a stock and commonly arise through exploration and evaluation.

g. Extractions are reductions in stock due to physical removal or harvest of an environmental asset through a process of production.

h. Mineral resources comprise known deposits of non-metallic minerals and metallic minerals.

i. Reappraisals reflect changes in the measured stock of assets due to the use of updated information that permits a reassessment of the size of the stock.

j. Reclassifications are changes in assets that result from situations in which an asset is used for a different purpose. A reclassification of an asset in one category should be offset by an equivalent reclassification in another category.

V. Dissemination of Results and Revision

The Mineral Accounts is released annually in the PSA website. The web release materials include press release and statistical tables.

Source: United Nations System of Environmental-Economic Accounting 2012 Central Framework

List of Tables

Nickel

Table 1.1 Physical Asset Account: Total Nickel Resources, 2013 to 2018

Table 1.2 Physical Asset Account: Class A Nickel Resources, 2013 to 2018

Table 1.3 Physical Asset Account: Class B Nickel Resources, 2013 to 2018

Table 1.4 Physical Asset Account: Class C Nickel Resources, 2013 to 2018

Table 1.5 Amount of Nickel Resources by Class, 2013 to 2018

Gold

Table 2.1 Physical Asset Account: Total Gold Resources, 2013 to 2018

Table 2.2 Physical Asset Account: Class A Gold Resources, 2013 to 2018

Table 2.3 Physical Asset Account: Class B Gold Resources, 2013 to 2018

Table 2.4 Physical Asset Account: Class C Gold Resources, 2013 to 2018

Table 2.5 Amount of Gold Resources by Class, 2013 to 2020

Copper

Table 3.1 Physical Asset Account: Total Copper Resources, 2013 to 2018

Table 3.2 Physical Asset Account: Class A Copper Resources, 2013 to 2018

Table 3.3 Physical Asset Account: Class B Copper Resources, 2013 to 2018

Table 3.4 Physical Asset Account: Class C Copper Resources, 2013 to 2018

Table 3.5 Amount of Copper Resources by Class, 2013 to 2018

Chromite

Table 4.1 Physical Asset Account: Total Chromite Resources, 2013 to 2018

Table 4.2 Physical Asset Account: Class A Chromite Resources, 2013 to 2018

Table 4.3 Physical Asset Account: Class B Chromite Resources, 2013 to 2018

Table 4.4 Physical Asset Account: Class C Chromite Resources, 2013 to 2018

Table 4.5 Amount of Chromite Resources by Class, 2013 to 2018

VI. Citation

Philippine Statistics Authority. (20 August 2020). Technical Notes on 2013 - 2018 Mineral Accounts.

https://psa.gov.ph/system/files/enrad/Press%2520Release%2520ao%252014Aug2020%2520final%2520signed.pdf

VII. Contact Information

Ms. Virginia M. Bathan

Chief Statistical Specialist

Environment and Natural Resources Accounts Division

(632) 8376-2041

enradstaff@gmail.com

For data request, you may contact:

Knowledge Management and Communications Division

(632) 8462-6600 locals 839, 833, and 834

info@psa.gov.ph

1 Mineral Accounts of the Philippines, Phil-WAVES Project, World Bank and Philippine Statistics Authority

2 United Nations System of Environmental-Economic Accounting 2012 Central Framework